Full Text (PDF)

Indian Journal of Forensic Medicine and Pathology 18((2 Suppl)):p 312-320, April-June 2025. | DOI: https://doi.org/10.21088/ijfmp.0974.3383.18225.33

Review Article

Forensic Accounting and Fraud Detection: A Systematic Literature Review and Prevention Methods

Dipti Singh, Manjeet Kumar, Parul Garg, Manuha Nagpal, Sunil Kumar Yadav

Author Information

Licence:

Attribution-Non-commercial 4.0 International (CC BY-NC 4.0)This license enables reusers to distribute, remix, adapt, and build upon the material in any medium or format for noncommercial purposes only, and only so long as attribution is given to the creator.

Indian Journal of Forensic Medicine and Pathology 18((2 Suppl)):p 312-320, April-June 2025. | DOI: https://doi.org/10.21088/ijfmp.0974.3383.18225.33

How Cite This Article:

Singh D, Kumar M, Garg P, et al. Forensic Accounting and Fraud Detection: A Systematic Literature Review and Prevention Methods. Indian J Forensic Med Pathol. 2025;18(2 Suppl):312-320.Timeline

Received : June 28, 2024

Accepted : June 28, 2025

Published : June 30, 2025

Abstract

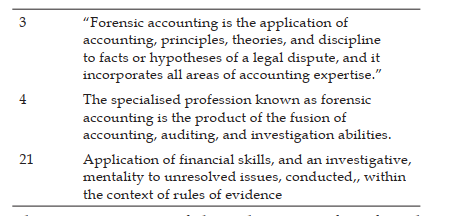

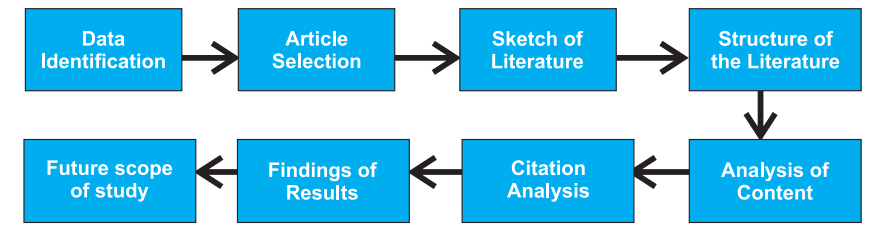

The aim of this study is to identify the role of forensic- accounting-that plays a vital role in, detecting & preventing fraud as well as to address pertinent investigation concerns. “Accounting principles, theories and procedures are applied in forensic accounting to analyse the problems in a legal way and contain every field of accounting.-.”Forensic> accounting< is a specialised area of accounting which includes auditing and investigative analytical skills.[4] Forensic accounting is required because corporate crises are happening more frequently all over the world. Financial fraud poses the greatest threat to the economy, making forensic accountants and traditional auditors crucial. Therefore, this study looks into fraud detection methods and ways to prevent it. In order to recognise and identify the current literature on forensic accounting and its preventative techniques, this study used the Preferred Reporting Method for Systematic Literature Reviews (SLR). It has been determined from this research that very few studies have analysed forensic accounting employing SLR techniques. This study also completes an integrated analysis with a concentration on three distinct areas: forensic accounting frauddetection, fraud prevention, methods & policy implementation.

References

- 1. Abdulrahman, S. “Forensic accounting and fraud prevention in Nigerian public sector: A conceptual paper.” International Journal of Accounting & Finance Review 4.2 (2019): 13-21.

- 2. Ademola, Lateef Saheed, Ayoib B. Ch-Ahmad, and Oluwatoyin Muse Johnson Popoola. “The forensic accountants’ skills and ethics on fraud prevention in the Nigerian public sector.” Academic Journal of Economic Studies 3.4 (2017): 77-85.

- 3. Brown, Phil A., Morris H. Stocks, and W. Mark Wilder. “Ethical exemplification and the AICPA Code of Professional Conduct: An empirical investigation of auditor and public perceptions.” Journal of Business Ethics 71 (2007): 39-71.

- 4. Akinbowale, Oluwatoyin Esther, Heinz Eckart Klingelhöfer, and MulatuFekaduZerihun. “The integration of forensic accounting and the management control system as tools for combating cyberfraud.” Academy of Accounting and Financial Studies Journal 25.2 (2021): 1-14.

- 5. Apostolou, Nicholas G., and Larry Crumbley. “The Expanding Role of the Forensic Accountant.” Forensic Examiner 14.3 (2005).

- 6. Atağan, Gülşah, and Aylin Kavak. “Relationship between fraud auditing and forensic accounting.” International Journal of Contemporary Economics & Administrative Sciences 7 (2017).

- 7. 7. Awolowo, Ifedapo. Financial statement fraud: The need for a paradigm shift to forensic accounting. Sheffield Hallam University (United Kingdom), 2019.

- 8. 8. Bhasin, Madan Lal. “Survey of skills required by the forensic accountants: Evidence from a developing country.” International journal of contemporary business studies 4.2 (2013).

- 9. Bhasin, Madan Lal. “Contribution of forensic accounting to corporate governance: An exploratory study of an Asian country.” International Business Management 10.4 (2015)

- 10. Bhavani, Ganga, Anupam Mehta, and Christian TabiAmponsah. “Forensic accounting education in the UAE.” Available at SSRN 2899481 (2016).

- 11. Caruana, Yanika, et al. “The effectiveness of forensic auditors in the insurance process.” (2020).

- 12. Chui, Lawrance, and Byron Pike. “Auditors’ responsibility for fraud detection: New wine in old bottles.” Journal of Forensic & Investigative Accounting 5.1 (2013): 204-233.

- 13. Chukwuma, O.V., J.I. Ugwu, and D.S. Babalola. “Application of forensic accounting in predicting the financial performance growth of MTN mobile communication in Nigeria.” Journal of Environmental Science and Economics 1.1 (2022): 67-76.

- 14. Enofe, A.O., G.A. Ekpulu, and T.O. Ajala. “Forensic accounting and corporate crime mitigation.” European Scientific Journal 11.7 (2015).

- 15. Gbegi, D.O., and J.F. Adebisi. “Forensic accounting skills and techniques in fraud investigation in the Nigerian public sector.” Mediterranean Journal of Social Sciences 5.3 (2014): 243-252. Dipti Singh, Manjeet Kumar, Parul Garg, et al. Forensic Accounting and Fraud Detection: A Systematic Literature Review and Prevention Methods320

- 16. Grima, Simon, and EnginBoztepe, eds. Contemporary issues in public sector accounting and auditing. Emerald Publishing Limited, 2021.

- 17. Grubor, Gojko, NenadRistić, and NatašaSimeunović. “Integrated forensic accounting investigative process model in digital environment.” International Journal of Scientific and Research Publications 3.12 (2013): 1-9.

- 18. Houck, Max M., et al. “Forensic accounting as an investigative tool.” The CPA Journal 76.8 (2006): 68.

- 19. Huber, Wm Dennis. “Forensic accounting, fraud theory, and the end of the fraud triangle.” Journal of Theoretical Accounting Research 12.2 (2017).

- 20. Kaur, Baljinder, Kiran Sood, and Simon Grima.“A systematic review on forensic accounting and its contribution towards fraud detection and prevention.” Journal of Financial Regulation and Compliance 31.1 (2022): 60-95.

- 21. Kurnaz, Niyazi, İbrahim KÖKSAL, and Tolga Ulusoy. “Forensic Accounting In Financial Fraud Control in Digital Environment: A Research on Independent Auditors.” Electronic Turkish Studies 14.3 (2019).

- 22. Mansor, Rabiu Abdullahi Noorhayati. “Forensic accounting and fraud risk factors: the influence of fraud diamond theory.” The American Journal of Innovative Research and Applied Sciences 7.28 (2015): 186-192.

- 23. Mukoro, Dickson. “The role of forensic accountants in fraud detection and national security in Nigeria.” Manager 17 (2013): 90-106.

- 24. Okoye, Emmanuel Ikechukwu, and D.O. Gbegi. “Forensic accounting: A tool for fraud detection and prevention in the public sector. (A Study of Selected Ministries in Kogi State).” Okoye, EI & Gbegi, DO (2013). Forensic Accounting: A Tool for Fraud Detection and Prevention in the Public Sector. (A Study of Selected Ministries in Kogi State). International Journal of Academic Research in Business and Social Sciences 3.3 (2013): 1-19.

- 25. Okpako, A.E., and E.N. Atube. “The impact of forensic accounting on fraud detection.”European Journal of Business and Management 5.26 (2013): 61-70.

- 26. Ozcan, Ahmet. The use of Beneish model in forensic accounting: evidence from Turkey.» Journal of Applied Economics and Business Research 8.1 (2018): 57-67.

- 27. Prabowo, Hendi Yogi. “Better, faster, smarter: developing a blueprint for creating forensic accountants.” Journal of Money Laundering Control 16.4 (2013): 353-378.

- 28. Sharma, Anuj, and Prabin Kumar Panigrahi. “A review of financial accounting fraud detection based on data mining techniques.” arXiv preprint arXiv: (2013); 1309.3944.

- 29. Wang, Jim, Grace Lee, and D. Larry Crumbley. “Current availability of forensic accounting education and state of forensic accountingservices in Hong Kong and mainland China.” Journal of Forensic and Investigative Accounting8.3 (2016): 515-534.

- 30. Johnson, Craig E. Ethics in the workplace: Tools and tactics for organizational transformation. Sage Publications, 2009.

Data Sharing Statement

There are no additional data available. All raw data and code are available upon request.

Funding

This research received no funding.

Author Contributions

All authors contributed significantly to the work and approve its publication.

Ethics Declaration

This article does not involve any human or animal subjects, and therefore does not require ethics approval.

Acknowledgements

We would like to express our gratitude to the patients, their families, and all those who have contributed to this study.

Conflicts of Interest

No conflicts of interest in this work.

About this article

Cite this article

Singh D, Kumar M, Garg P, et al. Forensic Accounting and Fraud Detection: A Systematic Literature Review and Prevention Methods. Indian J Forensic Med Pathol. 2025;18(2 Suppl):312-320.

Licence:

Attribution-Non-commercial 4.0 International (CC BY-NC 4.0)This license enables reusers to distribute, remix, adapt, and build upon the material in any medium or format for noncommercial purposes only, and only so long as attribution is given to the creator.

| Received | Accepted | Published |

|---|---|---|

| June 28, 2024 | June 28, 2025 | June 30, 2025 |

DOI: https://doi.org/10.21088/ijfmp.0974.3383.18225.33

Keywords

Fraud detectionForensicAccountingPrevention methodSLR techniqueSearch for Similar Articles

Similar Articles

- Pesticide Contamination in Indian Agricultural and Residential Areas: A Compara...

- Forensic Age Estimation using CBCT-Derived Mandibular Morphometrics: A Comparat...

- A 2 Years Retrospective Study of the Spectrum of Poisoning in a Tertiary Care C...

- Knowledge and Attitude of MBBS Students Regarding Post Mortem Examination: A Cr...

- Sudden Death in a 7-year-old Child Due to Neoplasm: A Case Report

Article Level Metrics

Last UpdatedWednesday 08 July 2026, 06:32:54 (IST)

7722

Accesses

56

2137

00

Citations

NA

NA

NA

Download citation

Article Keywords

Keyword Highlighting

Highlight selected keywords in the article text.

Timeline

| Received | June 28, 2024 |

| Accepted | June 28, 2025 |

| Published | June 30, 2025 |

licence

Attribution-Non-commercial 4.0 International (CC BY-NC 4.0)

This license enables reusers to distribute, remix, adapt, and build upon the material in any medium or format for noncommercial purposes only, and only so long as attribution is given to the creator.