Full Text (PDF)

Journal of Social Welfare and Management 15(3):p 105-113, September-December 2023. | DOI: http://dx.doi.org/10.21088/jswm.0975.0231.15323.1

Original Article

Disparities in Cost of Equity Estimation Among Estimation Models in the Indian Context

Author Information

Licence:

Attribution-Non-commercial 4.0 International (CC BY-NC 4.0)This license enables reusers to distribute, remix, adapt, and build upon the material in any medium or format for noncommercial purposes only, and only so long as attribution is given to the creator

Journal of Social Welfare and Management 15(3):p 105-113, September-December 2023. | DOI: http://dx.doi.org/10.21088/jswm.0975.0231.15323.1

How Cite This Article:

Unni N, Kumar SS. Disparities in cost of equity estimation among estimation models in the Indian context. J Soc Welfare Manag. 2023;15(3 Pt 1):105–13.Timeline

Received : June 20, 2023

Accepted : August 07, 2023

Published : December 12, 2023

Abstract

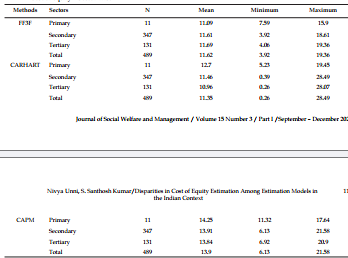

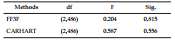

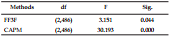

The purpose of this study is to bring out the disparities in the cost of equity of Indian companies estimated using the three asset pricing models such as the Capital Asset Pricing Model (CAPM), the Fama-French Three-Factor (FF3F) model, and the Carhart four-factor model. The stock price data of 489 companies listed in the National Stock Exchange (NSE) from 2012 to 2019 (8 years) were used for estimating the cost of equity capital. The coefficients of the factors in the models were estimated applying Ordinary Least Square (OLS) regression method. One-way ANOVA was used to examine the group-wise differences in the cost of equity. The computed cost of equity of Indian companies significantly differs among the three estimation models. Further, significant differences in the cost of equity were observed across industries in all three estimation models. Market capitalization-wise, differences in cost of equity were found as per CAPM and FF3F model. But no such differences were found in the case of Carhart's four-factor model. Sector-wise analysis doesn’t show differences in the cost of equity.

References

- 1. Laghi E, Di Marcantonio M. Beyond CAPM: estimating the cost of equity considering idiosyncratic risks. Quant Finance. 2016 Aug 2;16(8):1273–96.

- 2. Basiewicz PG, Auret CJ. Feasibility of the fama and french three factor model in explaining returns on the JSE. Investment Analysts Journal. 2010;71(1):13–25.

- 3. Sharpe WF. CAPITAL ASSET PRICES: A THEORY OF MARKET EQUILIBRIUM UNDER CONDITIONS OF RISK. J Finance. 1964;19(3):425– 42.

- 4. Lintner J. The Valuation of Risk Assets and the Selection of Risky Investments in Stock Portfolios and Capital Budgets [Internet]. Vol. 47. 1965. Available from: https://about.jstor.org/terms.

- 5. Galagedera DUA. A review of capital asset pricing models. Managerial Finance. 2007 Sep 4;33(10):821–32.

- 6. Moyo V. Inferring The Cost Of Equity: Does The CAPM Consistently Outperform The Income And Multiples Valuation Models? Vol. 34, The Journal of Applied Business Research.

- 7. Bornholt G. Extending the capital asset pricing model: The reward beta approach. Vol. 47, Accounting and Finance. 2007. p. 69–83.

- 8. Lee S, Upneja A. Is Capital Asset Pricing Model (CAPM) the best way to estimate cost-of-equity for the lodging industry? International Journal of Contemporary Hospitality Management. 2008;20(2):172–85.

- 9. Chiah M, Chai D, Zhong A, Li S. A Better Model? An Empirical Investigation of the Fama–French Five-factor Model in Australia. International Review of Finance. 2016 Dec 1;16(4):595–638.

- 10. Lalwani V, Chakraborty M. Multi-factor asset pricing models in emerging and developed markets. Managerial Finance. 2020 Mar 19;46(3):360–80.

- 11. Fama EF, French KR. Common risk factors in the returns on stocks and bonds*. Vol. 33, Journal of Financial Economics. 1993.

- 12. Gaunt C. Size and book to market effects and the Fama French three factor asset pricing model: evidence from the Australian stockmarket. Vol. 44, Accounting and Finance. 2004.

- 13. Faff R. A simple test of the Fama and French model using daily data: Australian evidence. Applied Financial Economics. 2004 Jan 15;14(2):83–92.

- 14. Simpson MW, Ramchander S. An inquiry into the economic fundamentals of the Fama and French equity factors. J Empir Finance. 2008 Dec;15(5):801– 15.

- 15. Vo DH. Which Factors Are Priced? An Application of the Fama French Three-Factor Model in Australia. Economic Papers. 2015 Dec 1;34(4):290– 301.

- 16. Carhart MM. On persistence in mutual fund performance. Journal of Finance. 1997;52(1):57–82.

- 17. Garyn-Tal S, Lauterbach B. The formulation of the four factor model when a considerable proportion of firms is dual-listed. Emerging Markets Review. 2015 Sep 1;24:1–12.

- 18. Rath S, Durand RB. Decomposing the size, value and momentum premia of the Fama-FrenchCarhart four-factor model. Econ Lett. 2015 Jul 1;132:139–41.

- 19. Khudoykulov K. Asset-pricing models: A case of Indian capital market. Cogent Economics and Finance. 2020 Jan 1;8(1).

- 20. Zaremba A, Czapkiewicz A, Szczygielski JJ, Kaganov V. An Application of Factor Pricing Models to the Polish Stock Market. Emerging Markets Finance and Trade. 2019 Jul 15;55(9):2039– 56.

- 21. Sreenu N. An Empirical Test of Capital Assetpricing Model and Three-factor Model of Fama in Indian Stock Exchange. Management and Labour Studies. 2018 Nov 1;43(4):294–307.

- 22. Xu J, Zhang S. The Fama-French Three Factors in the Chinese Stock Market. China Accounting and Finance Review. 2014 Jul;16(2).

- 23. Sehgal S, Balakrishnan A. Robustness of FamaFrench Three Factor Model: Further Evidence for Indian Stock Market. Vision: The Journal of Business Perspective. 2013 Jun;17(2):119–27.

- 24. Nartea G V., Ward BD, Djajadikerta HG. Size, BM, and momentum effects and the robustness of the Fama-French three-factor model: Evidence from New Zealand. International Journal of Managerial Finance. 2009 Apr 3;5(2):179–200.

- 25. Pal Taneja Y. Arumugam (1996) showed market anomaliesfor CAPM Fama French. Jagadeesh. Bhandari; 1977.

- 26. Soumaré I, Aménounvé EK, Diop O, Méité D, N’Sougan YD. Applying the CAPM and the FamaFrench models to the BRVM stock market. Applied Financial Economics. 2013 Feb;23(4):275–85.

- 27. Hirt GA, Block SB. Fundamentals of investment management. New York: Mcgraw-Hill/Irwin; 2012. Nivya Unni, S. Santhosh Kumar/Disparities in Cost of Equity Estimation Among Estimation Modelsin the Indian Context

- 28. Fama French and Momentum Factors: Data Library for Indian Market [Internet]. 2023 [cited 2020 May 25]. Available from: https://faculty.iima. ac.in/~iffm/Indian-Fama-French-Momentum/.

- 29. Groeneveld RA, Meeden G. Measuring Skewness and Kurtosis [Internet]. Vol. 33, Source: Journal of the Royal Statistical Society. Series D (The Statistician). 1984. Available from: https://about. jstor.org/terms.

Data Sharing Statement

There are no additional data available

Funding

This research received no funding

Author Contributions

All authors contributed significantly to the work and approve its publication.

Ethics Declaration

This article does not involve any human or animal subjects, and therefore does not require ethics approval

Acknowledgements

Information Not Provided

Conflicts of Interest

No conflicts of interest in this work.

About this article

Cite this article

Unni N, Kumar SS. Disparities in cost of equity estimation among estimation models in the Indian context. J Soc Welfare Manag. 2023;15(3 Pt 1):105–13.

Licence:

Attribution-Non-commercial 4.0 International (CC BY-NC 4.0)This license enables reusers to distribute, remix, adapt, and build upon the material in any medium or format for noncommercial purposes only, and only so long as attribution is given to the creator

| Received | Accepted | Published |

|---|---|---|

| June 20, 2023 | August 07, 2023 | December 12, 2023 |

DOI: http://dx.doi.org/10.21088/jswm.0975.0231.15323.1

Keywords

Asset Pricing ModelsFama-French Three-Factor Model;Carhart Four - Factor ModelSearch for Similar Articles

Similar Articles

- Legal and Technological Challenges of IPR in Digital Library Services

- Navigating the New India: Gen Z at the Intersection of Aspiration, Anxiety, and...

- A Comparative Analysis of Financial Performances of Sail and JSW Steel Company’...

- Tourism-Driven Local Business Growth and Economic Progress in Tirunelveli: An An...

- The Credential Crunch: Academic Degree Inflation and the Reimagining of Universi...

Article Level Metrics

Last UpdatedTuesday 07 July 2026, 06:23:41 (IST)

1163

Accesses

2

112

00

Citations

NA

NA

NA

Download citation

Article Keywords

Keyword Highlighting

Highlight selected keywords in the article text.

Timeline

| Received | June 20, 2023 |

| Accepted | August 07, 2023 |

| Published | December 12, 2023 |

licence

Attribution-Non-commercial 4.0 International (CC BY-NC 4.0)

This license enables reusers to distribute, remix, adapt, and build upon the material in any medium or format for noncommercial purposes only, and only so long as attribution is given to the creator