Full Text (PDF)

Journal of Social Welfare and Management 17(1):p 07-13, January-April 2025. | DOI: 10.21088/jswm.0975.0231.17125.1

Original Article

Impact of Consumer Preference for Housing Loan in HDFC Bank in Thoothukudi District

Author Information

Licence:

Attribution-Non-commercial 4.0 International (CC BY-NC 4.0)This license enables reusers to distribute, remix, adapt, and build upon the material in any medium or format for noncommercial purposes only, and only so long as attribution is given to the creator.

Journal of Social Welfare and Management 17(1):p 07-13, January-April 2025. | DOI: 10.21088/jswm.0975.0231.17125.1

How Cite This Article:

Amutha D. Impact of Consumer Preference for Housing Loan in HDFC Bank in Thoothukudi District. J Soc Welfare Manag. 2025;17(1):7–13.Timeline

Received : February 22, 2025

Accepted : April 18, 2025

Published : April 30, 2025

Abstract

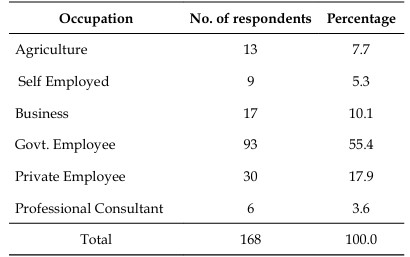

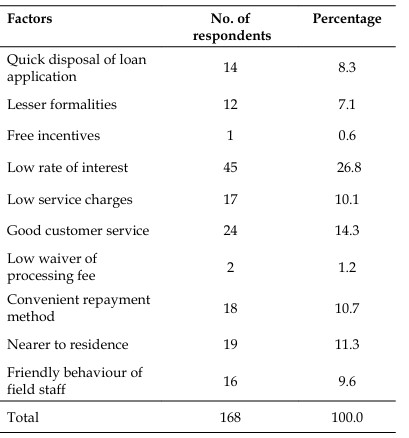

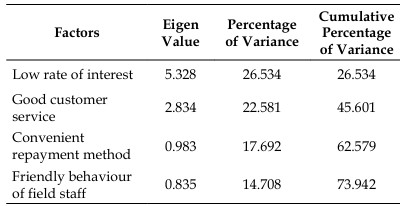

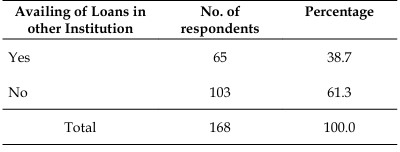

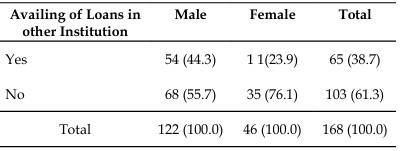

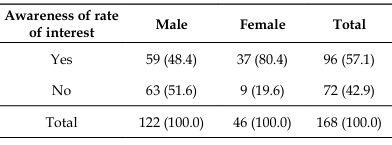

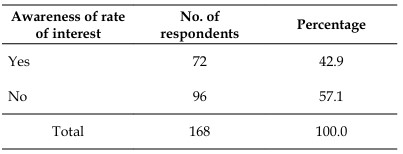

The housing industry is a significant contributor to the overall economic growth of the nation. There are over 269 different industries that are either directly or indirectly dependent on the housing sector. The primary objective of the study is to shed light on the characteristics of the housing loans that HDFC bank provides to customers in the Thoothukudi District. It entails gathering primary data from the borrowers who have taken out loans from HDFC bank in the Thoothukudi District. Some of the secondary data came from articles that were published in the IBA Bulletin and the RBI Bulletin, as well as pamphlets that were prepared by various banks. Accordingtothendingsofthestudy,elevenpercentofcustomershaveselected HDFC Bank because of its proximity to their place of residence; twenty-seven percent have selected the bank because of its low rate of interest; fourteen percent have selected the bank because of its excellent customer service; ten percent have selected the bank because of the friendly behaviour of field staff response; fourteen percent have selected the bank because of its prompt service; seven percent as a result As a result, it is evident that the interest rate that is provided by HDFC bank is a significant as pectthatin uences the borrowers’ decision to approach the bank.Accordingtothefindingsofthesurvey,itisclearthathouseloanborrowers prefer HDFC for a variety of reasons, including the speed with which their loan applications are processed, the reduced number of procedures required, the low interestrate, theexcellentcustomerservice, the exiblerepaymentmethod,and theniceconductoffieldworkers,amongotherreasons.Ontheotherhand, those who are interested in obtaining a home loan from HDFC in the study area face a few challenges. Following careful consideration of the recommendations made by the researcher, HDFC ought to take the appropriate actions to address the issues in ordertoimproveitsoverallperformance.Itispossibleforbankstoplayasignicant part in the process of encouraging the construction of homes in rural areas. Banks need to focus on mass customisation rather than mass market, and they also need to develop housing loan programs that are more dynamic and innovative.

References

- 1. Acharya, V.V; Hasan, I. and Saunders, A.(2002), “Should banks be diversified? Evidence from individual bank loan portfolios”, BIS Working Papers, No.118, September.13 JSWM / Volume 17 Number 1 / January – April 2025

- 2. Amutha, D. “A study of consumer awareness towards e-banking.” International journal of economics and management sciences 5.4 (2016): 350-353.

- 3. Amutha, D. “Growth of Demand and Time Deposits of Thoothukudi District Central CoOperative Bank.” AEIJMR – Vol 7 – Issue 01 – January 2019, ISSN - 2348 – 6724.

- 4. Amutha, D. and Laxmi, Muthu Maha, An Analysis of Deposits and Lending Behaviours of ICICI Bank (February 26, 2019). Available at SSRN: https://ssrn.com/abstract=3342489 or 10.2139/ssrn.3342489.

- 5. Avanindra Nath Thakur (2010) ‘Evolution of Banking’ Yojana Feb 2010, 38-40.

- 6. Costas Lapavitsas and Paulo L.Dos Santos (2008), “Globalization and Contemporary Banking on the Impact of New Technology”, contribution to political economy, 27, 31-56.

- 7. Deepak Satpathy (2014) Immediate Payment Systems as a catalyst for financial Deepening in Rural India. The Journal of Indian Institute of Banking & Finance 85(1), 21-24.

- 8. Dr Shekhar Kirani (2010) Don “t Let Fraud Ruin the promise of online banking in India, The Journal of Indian Institute of Banking & Finance 81(2) 5-6.

- 9. Jarunee Wonglimpiyarat (2006), “Technological change and Capabilities in Thai Banking”, International Journal of Financial Services Management. 1(2): 289-307.

- 10. Joicey Jose and Roy Jose (2013) Customer satisfaction research on ICICI Bank’s Hi-Tech banking services, special to Kanjirappally Branch, Journal of Commerce Research Journal 1(1), 1-9.

- 11. Kamesam Vepa. “Information Technology challenges to Banks.” Reserve Bank of India Bulletin, December 10, 2001.

- 12. Kapil Sheeba, (2004 ) “E-Banking; In Nascent Stage in India,” Professional Banker 4(8) 107.

- 13. Marcus, A. (2010), the contour of Information Technology and Indian Public Sector Banks’ growth, Banking-finance, 23(2). 15-19.

- 14. Philo Francis and Ms Shine Paul (2012) “A study on the usage of E-Banking Services in Thrissur, Journal of Organizational Management, 28(3), 38-43.

- 15. Private and Public Banks (Peter Kangis & Vassilis voukelatos, 1997). A comparison of the desires and attitudes of clients. Bank Marketing International Journal, 15(7), 279-287.

- 16. Uppal K. (2011) Internet banking in India: Emerging risks and new dimensions, Prime Journals Business Administration and Management (BAM) 1(3), 73-81.

- 17. Vasant Godse (2007) Banking on Technology. The Indian Context, The Journal of Indian Institute of Banking & Finance, 78 (2).

- 18. Venkatesvaran P. (2017) Technology Trends in the Indian Banking sector Journal of the management Accountant January 2017, 21 - 23.

Data Sharing Statement

There are no additional data available. All raw data and code are available upon request.

Funding

This research received no funding.

Author Contributions

All authors contributed significantly to the work and approve its publication.

Ethics Declaration

This article does not involve any human or animal subjects, and therefore does not require ethics approval.

Acknowledgements

We would like to express our gratitude to the patients, their families, and all those who have contributed to this study.

Conflicts of Interest

No conflicts of interest

About this article

Cite this article

Amutha D. Impact of Consumer Preference for Housing Loan in HDFC Bank in Thoothukudi District. J Soc Welfare Manag. 2025;17(1):7–13.

Licence:

Attribution-Non-commercial 4.0 International (CC BY-NC 4.0)This license enables reusers to distribute, remix, adapt, and build upon the material in any medium or format for noncommercial purposes only, and only so long as attribution is given to the creator.

| Received | Accepted | Published |

|---|---|---|

| February 22, 2025 | April 18, 2025 | April 30, 2025 |

DOI: 10.21088/jswm.0975.0231.17125.1

Keywords

Housing sectorEconomic developmenProperty rightsLoan schemesSearch for Similar Articles

Similar Articles

- Legal and Technological Challenges of IPR in Digital Library Services

- Navigating the New India: Gen Z at the Intersection of Aspiration, Anxiety, and...

- A Comparative Analysis of Financial Performances of Sail and JSW Steel Company’...

- Tourism-Driven Local Business Growth and Economic Progress in Tirunelveli: An An...

- The Credential Crunch: Academic Degree Inflation and the Reimagining of Universi...

Article Level Metrics

Last UpdatedTuesday 07 July 2026, 08:33:19 (IST)

1164

Accesses

6

112

00

Citations

NA

NA

NA

Download citation

Article Keywords

Keyword Highlighting

Highlight selected keywords in the article text.

Timeline

| Received | February 22, 2025 |

| Accepted | April 18, 2025 |

| Published | April 30, 2025 |

licence

Attribution-Non-commercial 4.0 International (CC BY-NC 4.0)

This license enables reusers to distribute, remix, adapt, and build upon the material in any medium or format for noncommercial purposes only, and only so long as attribution is given to the creator.